This summer marks the one-year anniversary of the paperback release of the book, “Blockchain Investor Manual: The Complete Guide to Blockchain Fundamentals, Trading and Investing.” Chapter 7, “A Blockchain Economy,” examined blockchain extensions and use cases beyond Bitcoin’s protocol, and Chapter 9, “Investing in Blockchain,” assessed the technology’s readiness and end-user acceptance for these applications. In a special three-part series for Forkast.News, authors Kosrow Dehnad and Joe Duncan revisit some of these applications based on their current readiness for adoption.

The series title, according to the authors, is a reference to the contrast between products such as non-fungible tokens (NFTs) and protocols like Dogecoin on the one hand, and blockchain’s more practical use cases on the other, where the technology’s utility — and hence, “seriousness” — has greater impact on more people.

This article focuses on how blockchain is transforming payments. Part 2 and Part 3, which will be published in the weeks to come, will explore blockchain use cases in social media and the internet of things (IoT).

_________________________________

Payments

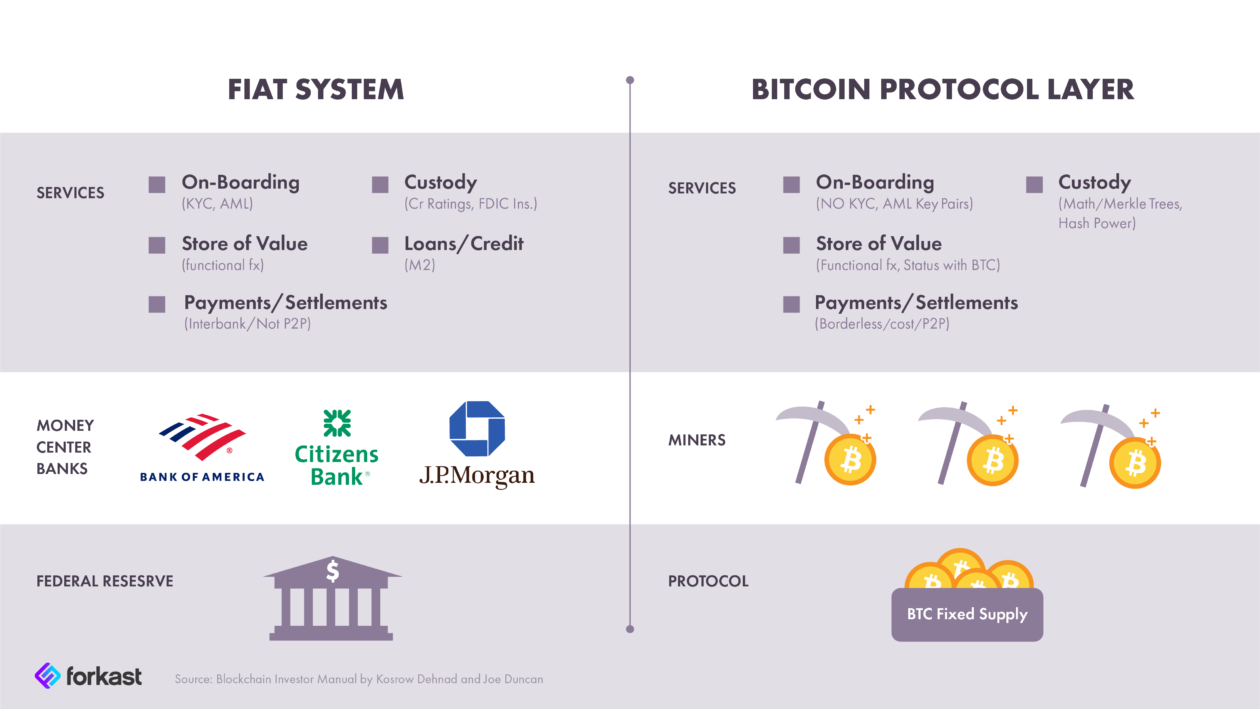

Here is a chart of Bitcoin to help visualize what can be done on-chain relative to the components of a fully built-out financial system.

Source: Blockchain Investor Manual

The lack of on-chain credit capability led us to highlight lending and liquidity providers as promising choices for investors due to their role in a build-out financial system, specifically citing the centralized finance (CeFi) lender BlockFi and DeFi exchange Uniswap, the latter prior to its own token listing in November. With the meteoric rise of projects like these and others underway, payments are becoming established as a core competency of blockchain technology in this serious stage.

On the one hand, the plethora of cryptocurrencies is reminiscent of the search engines at the beginning of the internet revolution where Google, Bing, Yahoo, Excite, AltaVista and others were all competing for the clicks of the users. Eventually, Google and Bing prevailed because of their “killer apps.” What could be a killer app for blockchain in payments to further drive adoption, and how could it happen?

The main functions of a currency are “medium of exchange,” “store of value” and “unit of ledger.” At this time, the main function of Bitcoin is “store of value” as well as means for financial speculation. However, a cryptocurrency that becomes a true medium of exchange will be a game-changer. Elon Musk gave that a try for a while by accepting Bitcoin as payment for Tesla automobiles. There have also been sporadic and anecdotal cases demonstrating that cryptocurrency can be accepted for the purchase of smaller items like pizza and coffee. Presumably, these use cases have lacked staying power due to some combination of holders not wanting to part with a store-of-value “savings asset,” transactions costs that can exceed bank and cross-border fees, and merchants’ hesitancy to accept a volatile form of payment relative to expenses denominated in their functional fiat currency.

A more efficient way of turning cryptocurrency into a medium of exchange is inversion, which we will explain by example. Consider a multinational conglomerate such as Pepsico that has operations all over the world and also owns Pizza Hut, Taco Bell and KFC restaurants. Pepsico could issue “Pepsicoin” with a value of US$1 and customers can pay for drinks, snacks and pizza at Pizza Hut and burritos at Taco Bell with either U.S. dollars or Pepsicoin. Furthermore, the company is prepared to issue new Pepsicoin if it appreciates above US$1 (similar to how a stablecoin like Tether is said to operate.) This way, Pepsicoin becomes a stablecoin and it also does not pose a serious threat to central banks because it does not replace their monetary policies. And, as far as Pepsico is concerned, it will have a negative cash cycle that is quite valuable: i.e., it is selling products forward and getting cash for them now.

One end-user application is that after a children’s soccer match, a parent might treat the team to dinner at Pizza Hut paid with the parent’s Pepsicoin or a designated amount sent to the child’s wallet. This payment system is not limited to local spending. Suppose a parent has an adult child who is traveling overseas, say to India, and the child goes to a KFC for lunch, the child can pay out of the parent’s wallet or with Pespsicoin sent to the child’s wallet. In such cases, the restaurant has to post its prices in Pepsicoin and local currency. If the U.S. dollar-Indian rupee exchange rate becomes very volatile, the price in Pepsicoin might have to be changed frequently.

A more practical approach is to keep Pepsicoin prices fairly stable and let the headquarters manage the foreign exchange risk, which they do anyway. Pepsicoin should particularly appeal to tourists because it removes the need of paying commission to convert their money to local currency. An additional benefit is that since Pepsicoin is purchased in U.S. dollars, if it becomes widely used, it will partially mitigate the issue of FX translation rate in the financial statements of Pepsico.

From a readiness standpoint, the relatively smooth operation of stablecoins like the custodial-based Tether, and even decentralized ones like MakerDAO, could now provide large consumer franchises with the comfort they need to launch their own branded products.

Let’s get silly

Although the purpose of this series of articles is to elaborate on use cases that are more likely to be widely accepted as “serious” in nature, let us not forget the important role of “silly” use cases in getting us to the point where we can see a broader array of real-world changes on the horizon.

The silly-sounding NFT project CryptoKitties, for example, was launched in 2017 in the gaming environment, where it faced minimal legacy hurdles to adoption. With the freedom to experiment, it broke much ground in demonstrating the value proposition of NFTs as assets with long-time horizons and that could be separated from the game from which they were created. Silly NFTs also helped to identify areas where blockchains were currently lacking in capacity to perform all the necessary functions, for example, image storage which is housed on the InterPlanetary File System. And just as sending the message, “hello,” from a computer on one coast to another laid the foundation for the expansion into the internet digital age, projects like CryptoKitties and Dogecoin are playing vital roles in ushering in the next major stage of decentralized global platforms that will transform the global economy across a wide range of economic and political spectrums.

In Part 2 in this series, we will review decentralized social media platforms. This use case cuts across important issues such as free speech, individual data ownership rights, and public versus private regulation. The demand for a decentralized solution is being accelerated across the globe by such events as mainland China’s censorship of pro-democracy communications in Hong Kong, and in the U.S. the recent banning of former U.S. President Donald Trump by Twitter and Facebook.