What is blockchain? And why does it matter?

Simply put, blockchain (a form of distributed ledger technology) scales trust.

If you were explaining why blockchain matters to your mother, you might tell her that she will no longer need to go through a bank to make a payment to the electric company. Or go to the Department of Motor Vehicles to transfer title for a car. Or instead of creating a paper will, she could fill out a digital will on a blockchain network. When certain criteria are met (such as when a grandchild reaches the right age), it would automatically divvy out inheritances. No executor needed.

On the other hand, if one were to explain why blockchain matters to a large financial institution, it would become apparent if implemented, that they might no longer need a large back office to support settlement and clearing, dramatically reducing costs.

In developing nations, blockchain will make it possible for subsistence farmers to get low cost crop insurance, so bad weather will no longer wipe out livelihoods or even entire communities.

It is the underlying technology behind Bitcoin that got us here.

Bitcoin and the Birth of Blockchain

In 2008, the Bitcoin network was introduced to the world by an anonymous programmer (or programmers) named Satoshi Nakomoto.

The goal of the Bitcoin network was to create a “peer-to-peer” network that empowered individuals around the globe by allowing them to exchange funds without a central authority.

Suddenly, there was another option to exchanging value. Those on the Bitcoin network did not need a bank, nor a middleman like Western Union. With Bitcoin, people could exchange funds person to person via your phone or computer. Andit was a groundbreaking idea.

And it struck a chord with individuals around the world who recognized that Bitcoin could be a way to escape flawed, centralized banking systems; like the global financial crisis of 2008, or today, where in Venezuela where hyperinflation has reduced how much the currency buys by almost 50% since 2015.

But the real game-changer was not the cryptocurrency called Bitcoin, but rather the blockchain network behind it. Where double-entry bookkeeping allowed capitalism to flourish, in the 21st century, blockchain is digital accounting where every transaction is verified by not one, nor two, but tens of thousands of people and computers around the world. It is a network effect that establishes trust and keeps it on the system. It allows peers to trust each other without a third-party. It is the blockchain network that allows Bitcoin to act as a peer-to-peer currency.

So how does blockchain technology work?

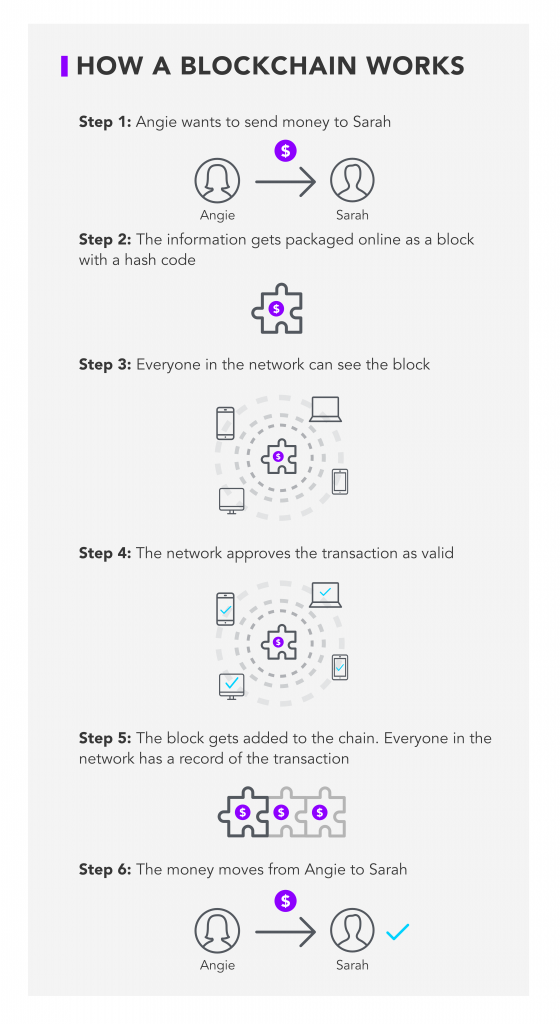

Blockchain 101: How a Blockchain Works

The simplest definition of a blockchain is a ledger shared across a network of computers.

When we say “ledger” we are talking about any electronic information like financial accounts, lists of purchases, medical records, etc.

This information is packaged and stored in a public database. You can think of this information as blocks and the public database as the chain.

Records are combined into blocks and added to the chain one after another.

While the above example was constructed to be as simple as possible, smart contracts can be as complex as any business logic that you can think of — which makes it incredibly promising to so many industries.

The blockchain is glued together by advanced cryptography and complex mathematics, that ensure the correctness of the information processed and stored. By adding an economic incentive for participants to honestly secure the network, it becomes increasingly financially unattractive to attack a system of a large enough size.

At the physical level, a blockchain network is a network of computers from all over the world. The computers compete to validate transactions by trying to solve complex mathematical puzzles. The winner receives an award in Bitcoin. The more computers that join, the more secure the network.

his process is known as “mining” and anyone with a computer can do it.

The resulting network is therefore not controlled by any one entity, but by the majority of the participating computers with aligned incentives, who decides which transactions to process and store. This means users do not need to delegate trust to a central and potentially vulnerable or ill-willed third party — it is “trustless.”

In practical terms, data becomes transparent that is neither controlled, nor can be changed by any central authority. The network governs and verifies itself.

Digital innovations of blockchain technology addresses issues that has arisen in our digital age.

- Blockchains boost security

Because they are distributed, blockchains offer benefits that traditional systems lack. In a normal network, it is possible for a hacker to take down a system by targeting its central point. Change that point, and you change the ledger. Since a blockchain is distributed across multiple points, it is far safer from these kinds of targeted attacks. - Blockchains can’t be altered

All of the parties involved with a blockchain have access to that blockchain. This makes it almost impossible to modify records or hide the truth. You change information without being found out almost immediately by the rest of the network. The presumption of possibility lies in the practicality of being successful in altering. One would have to control 51% of the nodes in existence to alter the blockchain. But in a decentralized environment where the number of nodes are constantly fluctuating, it would take an enormous amount of money to even start. The payoff would have to be 10x the return of that investment to “hack” the blockchain. We are talking millions of dollars.

While blockchain network has not been hacked, exchanges and wallets holding cryptocurrency have been hacked.

- Blockchain has multiple uses

Blockchain technology isn’t limited to peer-to-peer exchange.

Since blockchains can record all kinds of different data, industries today from travel to retail, insurance to pharmaceuticals are all exploring applications today.

The groundbreaking concepts that enable the management of data and assets at unprecedented levels of security, affordability, transparency (but also privacy) will change everything from how we pay and vote, to how we manage our identities, conduct business, and engage with others.

Over the last two years, blockchain technology has gained momentum. As of 2019, over 61% of digital firms have made investments into blockchain technology.

By 2025, the overall industry is estimated to be worth $28 billion.

We are only at the beginning of this enormous change that is to come.